Table of Contents (click to expand)

- One Globe, One Currency

- Smithsonian Agreement (1971)

- The Eurozone: A Real-World Experiment In Shared Currency

- Advantages Of Single Currency System

- Disadvantages Of Single Currency System

- So What Currency Does The World Actually Use Today?

- A Single Global Currency: Could It Happen By 2050?

- Why Is There No Global Currency Right Now?

The world doesn’t use one currency because national economies move at very different speeds, and a single global currency would force a single interest rate on countries facing opposite conditions. Nations would also lose the ability to devalue their own currency to absorb shocks, and there is no global authority to redistribute money between rich and poor regions, as the Eurozone debt crisis showed.

Wouldn’t it be so simple for us to shop online from US, UK, Indian, German, Australian or any other country’s websites without having to exchange our currency to theirs?

If everyone in the world used the same currency, education costs would be the same, so there would be less need to apply for scholarships. Why do the nations on our planet use different currencies?

One Globe, One Currency

When we say “one globe, one currency,” we mean that all nations on Earth should share the same economic and/or financial policies. However, different nations manage their finances and carry out their citizen-focused strategies in various ways. Some nations manage their finances too well, while other nations struggle in significant ways.

An Example To Understand The Concept Of A Global Currency

Imagine a family where each member has access to a single account, and anyone may use it however they choose to. The grandfather effectively manages all of his funds; he invests wisely in assets, doesn’t waste money, and has a proper flow of funds. In contrast, his grandson carelessly spends money on items that are not important, including game systems, expensive meals at upscale restaurants, and extravagant showpieces.

The grandson eventually abandons his obligation to repay his bills and recklessly shifts the burden onto others. Eventually, the grandfather, who personally committed no wrongdoing, is forced to pay for the large sums and incurs debt.

Now, this was a family example, but we may also use real-world examples.

Smithsonian Agreement (1971)

The last serious attempt at fixed, globally-coordinated exchange rates collapsed within living memory, so it is worth revisiting the wreckage. In August 1971, President Richard Nixon ended the convertibility of US dollars into gold, the so-called Nixon shock, breaking the back of the post-war Bretton Woods system.

To stitch things back together, the Group of Ten (G10) industrial nations (Belgium, Canada, France, Germany, Italy, Japan, the Netherlands, Sweden, the UK, and the US) met at the Smithsonian Institution in Washington on December 17–18, 1971, and announced what came to be called the Smithsonian Agreement. The deal devalued the US dollar by raising the official gold price from $35 to $38 per ounce (an 8.5% dollar devaluation), and other major currencies were revalued upward against the dollar. The combined effect was roughly a 10.7% average devaluation of the dollar against its trading partners.

That patch did not hold. Within about fifteen months, the Bretton Woods system collapsed entirely. On February 12, 1973, the US devalued the dollar by another 10%, pushing the official gold price up to $42.22 per ounce. (The Smithsonian Agreement, Federal Reserve History.) By March 1973, nearly all major currencies were floating freely against each other, and they have done so ever since.

The Eurozone: A Real-World Experiment In Shared Currency

You don’t need to imagine a single world currency in the abstract. A large slice of Europe has already tried something close to it. The euro launched as accounting money on January 1, 1999 with 11 founding countries, and physical euro notes and coins entered circulation on January 1, 2002. As of 2026, the eurozone has grown to 21 member states, with Croatia joining in 2023 and Bulgaria in 2026 (Britannica: Euro).

The euro has been a remarkable success at lowering transaction costs and binding member economies together. But it also exposed exactly why a global version is so hard. During the European sovereign debt crisis of 2010–2015, Greece’s public debt blew past 146% of GDP, and the European Central Bank had to set a single interest rate for both a booming Germany and a collapsing Greece. Greece could no longer devalue its own currency to regain export competitiveness, and the eurozone had no automatic fiscal-transfer mechanism to send help. The result was multiple Troika (European Commission, ECB, IMF) bailouts and years of austerity.

The lesson economists usually draw from this episode is that a monetary union without a fiscal union is fragile. A single currency works far better when its member regions share similar economic structures, allow workers to move freely between them, and have a central authority that can redistribute money from richer to poorer regions. Translate that to the entire planet, and you start to see why a single world currency is, charitably, a very long-term idea.

Advantages Of Single Currency System

There are some hypothetical advantages that could occur with a single currency system:

- Price clarity for consumers: A coffee in New York and a coffee in Tokyo would carry the same currency price, so you could compare costs across borders without a conversion app.

- No FX conversion fees: Companies and tourists currently bleed an estimated 1–5% on currency conversion at every step of a cross-border transaction. A single currency wipes that overhead out.

- Reduced exchange-rate risk: Exporters wouldn’t need to hedge against currency swings, which simplifies long-term contracts and investment.

- Fairer trade competition: Countries could no longer compete by deliberately weakening their currency (so-called competitive devaluation), and trade would be settled on goods and services alone.

Disadvantages Of Single Currency System

- Loss of monetary policy: Countries lose the ability to set their own interest rates or print money to respond to local downturns. If America falls into recession while Germany is booming, a one-size-fits-all global interest rate cannot help either.

- No devaluation as a shock absorber: Today, a country hit by a bad export year can let its currency fall, which makes its goods cheaper abroad and helps it recover. Under one currency, that lever disappears.

- Asymmetric impact across nations: Wealth gaps would widen, because poorer economies could no longer use a weak currency to attract investment and exports. Greece during the 2010 crisis is the textbook example.

- Political and sovereignty costs: Every country gives up a major chunk of national autonomy to a global central bank, which raises hard questions about who runs it and who answers to whom.

- Crisis contagion: A failure in one large member can drag the whole system down, since there is no escape valve in the form of an independent exchange rate.

So What Currency Does The World Actually Use Today?

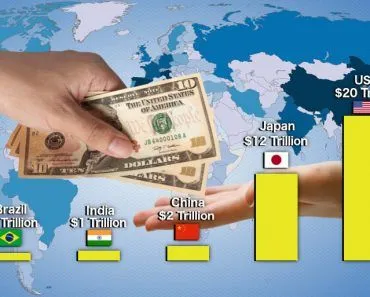

If there is no official world currency, you might assume every country’s money sits on equal footing. It doesn’t. In practice the world already leans heavily on one currency: the US dollar. Economists call it the world’s primary reserve currency, meaning it is the money that governments and central banks hold to settle international debts, anchor their own national currencies, and weather a crisis.

The numbers are lopsided. The dollar made up about 58% of disclosed global official foreign-exchange reserves in 2024, according to the US Federal Reserve, and roughly 57% in mid-2025 per the IMF, down from over 70% around the year 2000. The euro is a distant second at about 20%. The dollar also sits on one side of nearly 88% of all foreign-exchange trades (as of the Bank for International Settlements’ April 2022 survey), and it handles around half of international payments routed through the SWIFT network.

It dominates trade too. The Federal Reserve reports that, over 1999–2019, the dollar was used to invoice roughly 96% of trade in the Americas, 74% in the Asia-Pacific region, and 79% in the rest of the world (Europe being the exception, where the euro leads). In other words, a Brazilian exporter and a Korean importer who have nothing to do with the United States will often still strike their deal in dollars.

So the planet does have a de facto common currency for big international transactions, even without a single shared note in everyone’s wallet. What it lacks is a single currency that replaces the dollar, euro, yen, and rupee in everyday domestic life. That distinction, a dominant reserve currency versus one universal currency, is exactly why the dollar’s reach hasn’t settled the question of whether the world should keep its many national currencies.

A Single Global Currency: Could It Happen By 2050?

The dream of one global currency is not new. Back in 1969, economist Robert Mundell (who later won the Nobel Prize and is often called the “father of the euro”) argued for a world currency he nicknamed the INTOR. Even earlier, John Maynard Keynes had proposed an international reserve unit called the bancor at the 1944 Bretton Woods conference, but it was rejected in favor of a dollar-anchored system.

Today the closest things we have to a global money are the IMF’s Special Drawing Rights (SDRs), a basket of major currencies used between central banks, and a growing chorus of cryptocurrency advocates who argue that something like Bitcoin or a multi-CBDC (central bank digital currency) network could eventually serve as a borderless unit of account. Some futurists go further and predict an AI-managed, biometrics-linked global currency by 2050, though those predictions sit firmly in speculation, not economics.

Practically speaking, no serious central banker expects a single world currency by 2050. The Eurozone took half a century of integration and still wobbles. Scaling that experiment to 195 countries with vastly different incomes, institutions, and political systems is a much taller order.

Why Is There No Global Currency Right Now?

Economists usually answer this question by pointing to a concept called the Optimum Currency Area (OCA), proposed by Canadian economist Robert Mundell in 1961. Mundell argued that a shared currency only really works between regions that have (1) high labor mobility, (2) similar economic structures so that shocks hit them in similar ways, and (3) a shared fiscal authority that can move money from booming regions to struggling ones.

Lay those tests over the planet and they almost all fail. A worker in Tokyo can’t freely move to Lagos for a job. An oil-exporting economy and an oil-importing economy face exactly opposite shocks when crude prices swing. And no global authority exists to redistribute tax revenue from rich countries to poor ones. So the globe is currently too diverse to be governed by a single economic system. All nations therefore use free-floating (or managed-float) currencies, which lets each economy absorb shocks through its own exchange rate.

A single currency system simply doesn’t fit a planet of widely different economies. Floating currencies, for all their volatility, give each country a steering wheel of its own. Such a unified vision might be accomplished one day with deeper financial and political integration, but that day lies somewhere in the uncertain future.

References (click to expand)

- The Smithsonian Agreement. Federal Reserve History.

- Nixon and the End of the Bretton Woods System, 1971–1973. US Department of State, Office of the Historian.

- Euro. Britannica Money.

- The Greek sovereign debt crisis and the European Monetary Union. PubMed Central.

- 1973: The end of Bretton Woods, when exchange rates learned to float. Deutsche Bundesbank.

- Transcript of Economic Forum: One World, One Currency. International Monetary Fund.

- The International Role of the U.S. Dollar, 2025 Edition. Board of Governors of the Federal Reserve System.

- Dollar’s Share of Reserves Held Steady When Adjusted for FX Moves. International Monetary Fund (COFER).